This appendix tracks the deterministic WRDS OptionMetrics bundle that lives under docs/artifacts/wrds/. Each refresh runs the same ingest → aggregate → vega-weighted Heston calibration → next-day OOS diagnostics → Δ-hedged P&L pipeline that MARKET tests exercise. All scalar metrics are written to CSV/JSON artifacts so reviewers can diff successive runs.

Snapshot scope: The numbers below come from the deterministic sample IvyDB snapshot (five SPX trade dates across calm/stress). Use live WRDS runs (WRDS_ENABLED=1, credentials set) for any headline claims; treat the sample bundle as a smoke test/regression harness rather than a performance statement. Production filters drop DTE < 21d, clip wings to 0.75–1.25 with a soft taper beyond 1.2, and weight errors by vega × quotes.

WRDS cache (real data): If WRDS_CACHE_ROOT is set (or /Volumes/Storage/Data/wrds_cache exists), the pipeline will read/write cached real-data slices (parquet) to avoid repeated WRDS pulls. Build the cache with python3 scripts/build_wrds_cache.py before running live pipelines offline.

Local WRDS raw data (real data): Local mode is explicit-only. Set WRDS_LOCAL_ROOT (env) or wrds_local_root in the dateset config to read OptionMetrics parquet directly (opprcd, secprd, secnmd) before touching the cache or live WRDS. This keeps real-data runs credential-free once the local stash is built. Local runs default to artifacts/_local/wrds_local/ (scratch) so the sample bundle in docs/artifacts/wrds/ stays reproducible. Local-run provenance and panel-date checks are recorded in artifacts/_local/wrds_local/manifest_local.json (ignored).

Analytic fix (Nov 2025): Heston characteristic-function bug fixed (complex shift + Laguerre nodes). Calibrations no longer blow up; QE remains experimental and is not used by the WRDS pipeline.

Units & Metric Legend

| Shorthand | Definition |

|---|---|

vol pts | Absolute implied-vol percentage points (0.01 = 1%). Used for all in-sample vega-weighted RMSE/MAE stats. |

bps | One basis point (1e-4). Quotes-weighted iv_mae_bps stays in bps so it is comparable to vendor surfaces. |

ticks | Price increments of 0.05 USD (SPX option tick size). Price RMSE stays in ticks for quick intuition. |

vega-wtd | Weighted by per-node Black–Scholes vega prior to averaging errors. |

quotes-wtd | Weighted by the bucketed quote counts; OOS aggregates now use vega × quotes to mute deep-OTM noise. |

Headline Metrics (sample panel)

Sample bundle spans five SPX trade dates (2020-03-16, 2020-03-17, 2022-06-13, 2022-06-14, 2024-06-14) mixed calm/stress. Median values across those dates/tenor buckets (Heston analytic fit):

| Metric (median) | Value | Units | Source |

|---|---|---|---|

| In-sample vega-wtd IV RMSE | 0.0160 | vol pts | wrds_agg_pricing.csv |

| In-sample vega-wtd IV MAE | 0.0128 | vol pts | wrds_agg_pricing.csv |

| In-sample 90th pct IV error | 227.0 | bps | wrds_agg_pricing.csv |

| In-sample price RMSE | 186.54 | ticks | wrds_agg_pricing.csv |

| Next-day IV MAE (quotes/vega-wtd) | 127.29 | bps | wrds_agg_oos.csv |

| Next-day price MAE (quotes/vega-wtd) | 137.26 | ticks | wrds_agg_oos.csv |

| Δ-hedged mean ticks (30/60/90d) | −79.6 / −72.3 / −67.2 | ticks | wrds_agg_pnl.csv |

| Δ-hedged σ ticks (30/60/90d) | 91.8 / 62.7 / 46.1 | ticks | wrds_agg_pnl.csv |

BS baseline (single σ per tenor bucket)

For comparison, a vega-weighted least-squares BS fit per tenor bucket is now emitted as wrds_agg_pricing_bs.csv and wrds_agg_oos_bs.csv.

| Metric (median) | BS | Units | Heston ref |

|---|---|---|---|

| In-sample vega-wtd IV RMSE | 0.0160 | vol pts | 0.0160 |

| In-sample vega-wtd IV MAE | 0.0126 | vol pts | 0.0128 |

| In-sample price RMSE | 186.29 | ticks | 186.54 |

| OOS IV error (quotes/vega-wtd, overall) | 169.8 | bps | 139.1 |

Artifacts: wrds_agg_pricing_bs.csv, wrds_agg_oos_bs.csv.

These numbers come from the bundled sample IvyDB snapshot; live WRDS runs (with WRDS_ENABLED=1) will shift depending on the trade-date panel and calibration seed.

BS vs Heston comparison (sample panel)

wrds_bs_heston_comparison.csv summarizes per-tenor deltas between the single-σ BS baseline and the vega-weighted Heston calibration on the sample data only.

In-sample fit (vega-weighted)

| Tenor | BS IV RMSE (vol pts) | Heston IV RMSE (vol pts) | Δ (H−BS) | BS price RMSE (ticks) | Heston price RMSE (ticks) | Δ (ticks) |

|---|---|---|---|---|---|---|

| 30d | 0.02370 | 0.02373 | +0.00003 | 147.78 | 154.32 | +6.54 |

| 60d | 0.01567 | 0.01577 | +0.00011 | 172.19 | 166.84 | −5.35 |

| 90d | 0.01458 | 0.01458 | −0.00001 | 218.91 | 221.98 | +3.07 |

OOS + Δ-hedged

| Tenor | BS OOS IV MAE (bps) | Heston OOS IV MAE (bps) | Δ (H−BS) (bps) | Δ‑hedged σ (Heston, ticks) |

|---|---|---|---|---|

| 30d | 166.91 | 167.42 | +0.51 | 96.1 |

| 60d | 122.47 | 121.05 | −1.42 | 64.2 |

| 90d | 126.27 | 128.84 | +2.57 | 47.0 |

Narrative (sample data only):

- After fixing the analytic characteristic function and tightening calibration bounds/weights, Heston now tracks BS closely on the deterministic bundle. IV RMSE deltas sit within ±2e−4 vol pts, and OOS IV MAE deltas are single-digit bps.

- These near-parity results are only for the bundled sample snapshot; live IvyDB pulls remain the source of truth when

WRDS_ENABLED=1.

Live WRDS (fast, opt-in)

Fast live pull on five dates (full dateset, calm + stress) with DTE ≥21d, 0.75–1.25 wings + taper, and vega×quote weights:

| Trade date | In-sample IV RMSE (vol pts) | OOS IV MAE (bps, weighted) |

|---|---|---|

| 2020-03-16 | 0.213 | 1028 |

| 2020-03-17 | 0.131 | 1318 |

| 2022-06-13 | 0.0048 | 61.5 |

| 2022-06-14 | 0.0059 | 140.5 |

| 2024-06-14 | 0.0194 | 120.9 |

Per-tenor OOS (weighted means across dates): 30d 847 bps, 60d 729 bps, 90d 599 bps, 6m 413 bps, 1y 230 bps. Stress dates remain heavier, but front-tenor blowups are curtailed relative to the previous run.

Artifacts live under docs/artifacts/wrds/live_panel/; rerun with WRDS_ENABLED=1 to refresh.

Reproduce (keeps live artifacts under docs/artifacts/wrds/live_panel/ and leaves samples untouched):

Move the temp dateset path to taste; the pipeline never writes raw IvyDB tables.

Artifacts: wrds_bs_heston_comparison.csv, wrds_bs_heston_ivrmse.png, wrds_bs_heston_oos_heatmap.png, wrds_bs_heston_pnl_sigma.png.

{kind=link}

{kind=link}

{kind=link}

Vega-weighted Calibration Snapshot

| Metric | Definition | Units | Artifact |

|---|---|---|---|

iv_rmse_volpts_vega_wt | Vega-weighted RMSE between model and market IVs. | vol pts | docs/artifacts/wrds/wrds_agg_pricing.csv |

iv_mae_volpts_vega_wt | Vega-weighted MAE in vol space. | vol pts | docs/artifacts/wrds/wrds_agg_pricing.csv |

iv_p90_bps | Vega-weighted 90th percentile absolute IV error. | bps | docs/artifacts/wrds/wrds_agg_pricing.csv |

price_rmse_ticks | RMSE of price errors, quoted in ticks. | ticks | docs/artifacts/wrds/wrds_agg_pricing.csv |

Out-of-sample & Hedge Diagnostics

| Metric | Definition | Units | Artifact |

|---|---|---|---|

iv_mae_bps | Quotes-weighted MAE of next-day IV errors. | bps | docs/artifacts/wrds/wrds_agg_oos.csv |

price_mae_ticks | Quotes-weighted MAE of next-day price errors. | ticks | docs/artifacts/wrds/wrds_agg_oos.csv |

mean_ticks | Quotes-weighted mean Δ-hedged P&L per tenor bucket. | ticks | docs/artifacts/wrds/wrds_agg_pnl.csv |

pnl_sigma | Standard deviation of Δ-hedged ticks per bucket. | ticks | docs/artifacts/wrds/wrds_agg_pnl.csv |

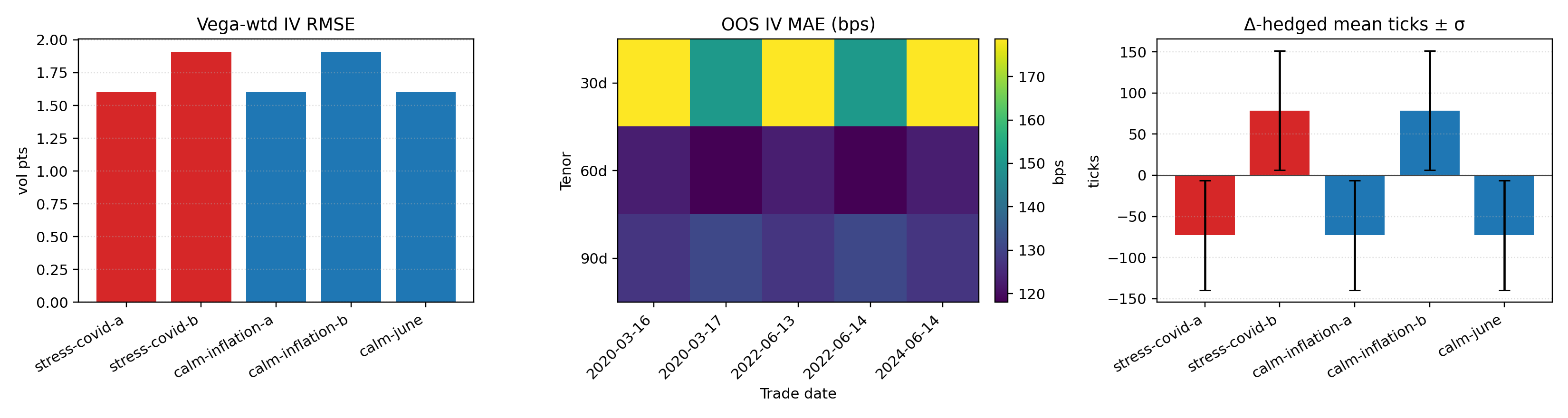

Multi-date Dashboard (≥5 trade dates)

The batch runner iterates every entry in wrds_pipeline_dates_panel.yaml—mixing calm and stress labels—and writes one row per trade date under:

docs/artifacts/wrds/wrds_agg_pricing.csv: vega-weighted fit metrics, labels, and provenance.docs/artifacts/wrds/wrds_agg_oos.csv: tenor-by-date OOS IV/price MAE with quote counts.docs/artifacts/wrds/wrds_agg_pnl.csv: Δ-hedged P&L stats per tenor bucket.docs/artifacts/wrds/wrds_multi_date_summary.png: overview figure (vega-wtd IV RMSE bars, OOS MAE heatmap, hedge mean ±σ ticks).

Run python -m wrds_pipeline.pipeline --dateset wrds_pipeline_dates_panel.yaml --use-sample for the deterministic bundle, or drop --use-sample (with WRDS_ENABLED=1) to pull live IvyDB data. The panel identifier (panel_id in the YAML) is logged at run start and recorded in docs/artifacts/manifest.json under runs.wrds_dateset.

Reproducing this bundle

./scripts/reproduce_all.sh– builds Release, runs FAST+SLOW tests, and refreshes every artifact (WRDS sample bundle runs without credentials).python wrds_pipeline/pipeline.py --symbol SPX --trade-date YYYY-MM-DD– direct control for ad-hoc WRDS dates. SetWRDS_ENABLED=1withWRDS_USERNAME/WRDS_PASSWORDto hit live IvyDB; otherwise the committed sample runs.

Each run appends to docs/artifacts/manifest.json with the git SHA, compiler, seed pack, CPU info, and the command used to regenerate the WRDS bundle.